Matheson & Co., Limited, established in London in 1848, is a wholly owned subsidiary of Jardine Matheson Holdings Limited. Jardine Matheson is today a diversified investment company focused principally on Asia.

The Group's interests include Hongkong Land, DFI Retail Group, Mandarin Oriental, Jardine Pacific, Jardine Cycle & Carriage and Astra, while the Group also has a minority interest in Zhongsheng Group, one of mainland China's major motor dealership groups. These companies are leaders in the fields of motor vehicles and related operations, property investment and development, food retailing, home furnishings, engineering and construction, transport services, restaurants, luxury hotels, financial services, heavy equipment, mining and agribusiness. Matheson & Co provides support services to the Group's subsidiary and associated companies, including its United Kingdom-based business interests.

Through its subsidiary, Mandarin Oriental – which operates some of the world's most prestigious hotels and resorts – Jardine Matheson’s UK interests include the Mandarin Oriental Hyde Park Hotel, one of London's most prestigious hotels located in the heart of Knightsbridge and the boutique Mandarin Oriental Mayfair.

Matheson & Co., Limited is a company registered in England and Wales.

Company Registration Number: 100295

Registered Office:

12 Upper Grosvenor Street

London, Mayfair

W1K 2ND

United Kingdom

Tel: 020 7816 8100

Corporate tax: 11630 51016

VAT registration: 233 7865 86

In accordance with Schedule 19 of the Finance Act 2016, we set out below the tax strategy of Matheson & Co., Limited. ("the Company"). We believe that this strategy constitutes good corporate practice in the area of UK tax management and tax transparency, while balancing the interests of our stakeholders.

Overall commitment

The Company will comply with its tax obligations which include making all appropriate returns covering all areas of UK taxes and ensuring the correct amounts of UK taxes are made by the due dates.

Working with the HMRC

The Company will maintain an open and transparent relationship with HMRC.

Tax risk management

When interpretation of the law is uncertain, the Company will seek to discuss the issue with HMRC at the time or refer to it when tax returns are filed. External advice will also be sought on matters of uncertainty or where there is no relevant specialist knowledge or experience in-house.

The Company operates a risk-based system of controls, processes and training in order to manage tax risks and minimise instances of error. The Company has a low tolerance for tax uncertainty.

Approach to tax planning

The Company adopts a prudent and low risk approach in tax planning. It will only utilise tax planning measures and opportunities for obtaining tax efficiencies where these comply with tax legislation, and when such tax planning is aligned with the commercial and economic activities of the Company. The Company will not use artificial structures that are intended for tax avoidance without bona fide business purpose, have no commercial substance or do not meet the generally understood intention of UK or international law.

The Company has a zero-tolerance policy towards tax evasion, any deliberate concealment of taxable income and benefits, or facilitating others in undertaking such activities.

Corporate governance

The finance director manages the Company's tax function and consults with the tax team of its global parent company. The finance director ensures that the Company adopts the appropriate tax accounting treatment and reporting standards. The Board has ultimate responsibility for the Company's tax policies and ensuring its principles and approach are adhered to.

The Company follows the wider Jardine Group's Group Policy Manual and Code of Conduct to which all employees are required to subscribe and held to the highest standard.

The above document has been approved by the Board of Directors on behalf of the Company and applies for the year to 31 December 2019 and subsequent periods. The Company's tax strategy (which will be reviewed at least annually) will remain in effect until any amendments are approved by the Board of Directors.

December 2025

June 2024

Introduction

1. This document is the Statement of Investment Principles (the "SIP") made by the Trustees of the Matheson Group Pension Plan (the "Plan") in accordance with the requirements of Section 35 of the Pensions Act 1995 (as amended by the Pensions Act 2004 and regulations made under it). The Plan is a defined benefit (DB) plan which is closed to future accrual since 2009.

2. The Trustees will review this SIP at least every three years to coincide with the triennial Actuarial Valuation or other actuarial advice relating to the statutory funding requirements. Furthermore, the Trustees will review this SIP without delay after any significant change in investment policy. Before finalising this SIP, the Trustees took advice from a suitably qualified firm and consulted Matheson & Co Ltd (the "Company"). The ultimate power and responsibility for deciding investment policy, however, lies solely with the Trustees.

Investment objectives

3. The Trustees have the following investment objectives:

4. While this is articulated as an agreed objective for the Plan to be fully funded on the Technical Provisions basis, the Trustee's ultimate goal is to be fully funded on a more prudent low-risk liability measure and subsequently on a solvency basis.

Investment strategy

5.The Trustees have agreed a long-term investment strategy that targets an expected return of Gilts +1.5% pa. Based on analysis as at 30 April June 2024, this level of return was expected to achieve full-funding on a low-risk liability measure (i.e., liability cashflows discounted at Gilts +0.5% pa) by 2026.

6. The Trustees have determined their investment strategy after considering the Plan's liability profile and requirements of the current Statutory Funding Objective, their own appetite for risk, the views of the Company on investment strategy, the Company's appetite for risk, and the strength of the Company's covenant as well as reflecting the Trustees' desire to diversify risk exposures and to manage their investments effectively. The Trustees received advice to determine the investment strategy for the Plan.

7. The investment strategy makes use of three key types of investments:

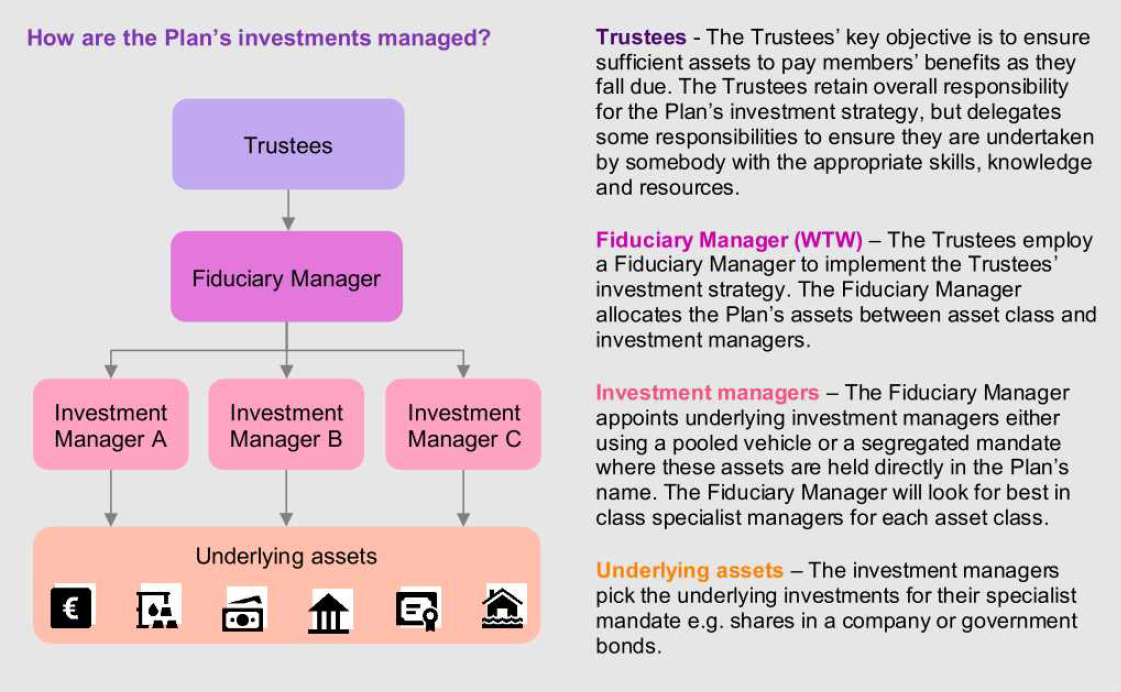

8. The Trustees have appointed an investment manager to manage the Plan's assets on a discretionary basis and to provide investment advisory services to the Trustees (the "Fiduciary Manager"). The balance within and between these investments will be determined from time to-time at the discretion of the Fiduciary Manager, with the objective of maximising the probability of achieving the Plan's investment strategy set by the Trustees, subject to maintaining risk within a limit agreed by the Trustees. The Fiduciary Manager's discretion is subject to guidelines set by the Trustees in the Fiduciary Management Agreement between the parties as amended from time to time (the "FMA"). In exercising investment discretion, the Fiduciary Manager is required to act in accordance with its obligations in the FMA, including the guidelines and any investment restrictions set out therein, and in so doing is expected to give effect so far as reasonably practicable to the principles contained in this SIP. This ensures appropriate incentivisation and alignment of decision-making with the Trustees' overall objectives, strategy and policies.

9. The implied initial Gilts +1.5% pa target portfolio to be managed by the Fiduciary Manager is set out below:

Asset Class | Initial Target |

| Liability Matching | 67%* |

| Secure Income | 11% |

| Diversified Return Seeking | 22% |

*The liability matching allocation uses leverage to deliver a target liability hedge ratio of 96% (as a percentage of assets). The Fiduciary Manager is required under its guidelines to maintain this ratio between 80% and 100%.

10. The Trustees may also consider opportunities to purchase bulk annuity policies as appropriate within the context of the Plan's investment strategy. Any bulk annuity policies fall outside the remit of the Fiduciary Manager's discretion.

11. The Plan will hold assets in cash and other money market instruments from time to time as may be deemed appropriate.

12. The Trustees will monitor the liability profile of the Plan and will regularly review, in conjunction with the Fiduciary Manager and the Scheme Actuary, the appropriateness of its investment strategy.

13. The expected return of all the Plan's investments will be monitored regularly and will be directly related to the Plan's investment objective.

14. The Trustees' policy is that there will be sufficient investments in liquid or readily realisable assets to meet cash flow requirements in foreseeable circumstances so that the realisation of assets will not disrupt the allocation of the Plan's overall investments, where possible. The Trustees have set explicit liquidity provisions in the Fiduciary Manager's guidelines as follows:

Time Frame | % of total plan assets |

| % realisable within 2 weeks | Minimum 55 |

% realisable within 1 month | Minimum 55 |

| % realisable within 1 year | Minimum 80 |

Investment managers

15. The Trustees have delegated investment selection, de-selection and the ongoing management of relationships with investment managers to the Fiduciary Manager within guidelines set by the Trustees in the FMA. Investments are made by the Fiduciary Manager on behalf of and in the name of the Trustees.

16. The Trustees consider the Fiduciary Manager's performance in carrying out these responsibilities as part of its ongoing oversight of the Fiduciary Manager. The Trustees expect the Fiduciary Manager to ensure that the Plan's investment portfolio, in aggregate, is consistent with the policies set out in this SIP, in particular those required under regulation 2(3)(b) of the Occupational Pension Schemes (Investment) Regulations (2005). The Trustees expects the Fiduciary Manager to check that the investment objectives and guidelines of any pooled vehicle are consistent with the Trustees' policies contained in the SIP.

17. WTW has been appointed as Fiduciary Manager since 2022. In accordance with the Financial Services and Markets Act 2000, the selection of specific investments will be delegated to investment managers. The investment managers will provide the skill and expertise necessary to manage the investments of the Plan competently. The duration of the arrangements with investment managers will be determined on an individual basis considering the nature of the relevant investment mandate. In most cases, managers are appointed with the expectation of a long-term relationship but with an ability to terminate where considered appropriate. However, there may be occasions when managers are put in place for a short period or a fixed period, depending on the nature of the investment strategy.

18. The Trustees and Fiduciary Manager are not involved in the investment manager's day-to-day method of operation and do not directly seek to influence attainment of their performance targets. However, the Fiduciary Manager may provide investment recommendations to the investment managers of certain pooled funds appointed where it considers it appropriate. The Fiduciary Manager will maintain processes to ensure that performance and risk are assessed on a regular basis against measurable objectives for each investment manager, consistent with the achievement of the Plan's long term objectives.

19. The Trustees expect the Fiduciary Manager to select investment managers with an expectation of a long-term partnership with the Trustees. which encourages active ownership of the Plan's assets. When assessing an investment manager's performance, the Trustees expect the Fiduciary Manager to focus on longer-term outcomes, commensurate with the Trustees' position as a long term investor. Consistent with this view, the Trustees do not expect that the Fiduciary Manager would terminate an investment based purely on short-term performance but recognises that an investment may be terminated within a short timeframe due to other factors such as a significant change in the relevant manager's business structure or investment team. The Trustees adopt the same long term focus as part of its ongoing oversight of the Fiduciary Manager.

20. For most of the Plan's investments, the Trustees expect the Fiduciary Manager to select investment managers with a medium to long time horizon, consistent with that of the Plan. In particular areas such as equity and credit, the Trustees expect the Fiduciary Manager to work with investment managers who will use their engagement activity to drive improved performance over medium to long term periods within the wider context of long-term sustainable investment. The Trustees note that the Fiduciary Manager may invest in certain strategies where such engagement is not deemed appropriate or possible, due to the nature of the strategy and/or the investment time horizon underlying decision making. The Trustees expect that the appropriateness of the Plan's allocation to such mandates is determined in the context of the Plan's overall objectives.

21. The Trustees recognise that an investment's long-term financial success is influenced by a range of financially material factors including environmental, social and governance ("ESG") issues.

22. Consequently, the Trustees (through the selection of the Fiduciary Manager with its approach to ESG issues as set out in the relevant paragraphs below) seek to be an active long-term investor. The Trustees' focus is explicitly on financially material factors. The Trustees· policy at this time is not to take into account non-financial matters in the selection, retention, and realisation of investments.

23. When considering their policy in relation to stewardship including engagement and voting, the Trustees expect investment managers to address broad ESG considerations taking into account the nature of the assets held under the relevant investment mandate, but has Identified climate and human and labour rights as key areas of focus for the Trustees. The Trustees assess that ESG risks, and in particular climate change, pose a financial risk to the Plan and that focussing on these issues is ultimately consistent with the Trustees' fiduciary duties and the financial security of their members. Whilst the Trustees' policy is to delegate several stewardship activities to the Fiduciary Manager and their investment managers, the Trustees recognise that the responsibility for these activities remains with the Trustees. The Trustees incorporate an assessment of how well the Fiduciary Manager and investment managers exercise these responsibilities as part of their overall assessment of their performance.

24. The Fiduciary Manager has a dedicated sustainable investment resource and a network of subject matter experts. The consideration of ESG issues is fully embedded in the investment manager selection and portfollo management process, with oversight undertaken on a periodic basis. The Trustees expect the Fiduciary Manager to assess the alignment of each investment manager's approach to sustainable investment (including engagement) with its own before making an investment on the Plan's behalf. The Trustees expect the Fiduciary Manager to engage with the Plan's investment managers where the Fiduciary Manager considers this appropriate regarding their approach to stewardship with respect to relevant matters including capital structure of investee companies, actual and potential conflicts, other stakeholders and ESG impact of underlying holdings. In addition, the Trustees expect the Fiduciary Manager to review the investment managers' approach to sustainable investment (including engagement) on a periodic basis and engage with the investment managers to encourage further alignment as appropriate.

25. The Fiduciary Manager considers a range of sustainable investment factors, such as, but not limited to, those arising from ESG considerations, including climate change, in the context of a broader risk management framework. The degree to which these factors are relevant to any given strategy is a function of time horizon, investment style, philosophy and particular exposures which the Fiduciary Manager takes into account in the assessment.

26. The Fiduciary Manager encourages and expects the Plan's investment managers to sign up to local or other applicable stewardship codes, in keeping with good practice, subject to the extent of materiality for certain asset classes. The Fiduciary Manager itself is a signatory to the Principles for Responsible Investment and the UK Stewardship Code and is actively involved in external collaborations and initiatives.

27. The Trustees' policy is to delegate responsibility for the exercising of rights (including voting rights) attaching to the Plan's investments to their investment managers. The Fiduciary Manager assesses the voting policies of the investment managers that it appoints on the Trustees' behalf, for consistency with the Trustees' policies and objectives, as appropriate. The Fiduciary Manager has also appointed EOS at Federated Hermes to undertake public policy engagement and company-level engagement on its behalf. EOS at Federated Hermes also assists the Trustees' equity managers with voting recommendations.

28. The Trustees expect the Fiduciary Manager to consider the fee structures of investment managers and the alignment of interests created by these fee structures as part of its investment decision making process, both at the initial selection of an investment manager and on an ongoing basis. Investment managers are generally paid an ad valorem fee, in line with normal market practice, for a given scope of services which includes consideration of long-term factors and engagement. The Trustees expect the Fiduciary Manager to review and report on the costs incurred in managing the Plan's assets regularly, which includes the costs associated with portfolio turnover. In assessing the appropriateness of the portfolio turnover costs at an individual investment manager level, the Trustees expects the Fiduciary Manager to have regard to the actual portfolio turnover and how this compares with the expected turnover range for that mandate.

Other matters

29. The Plan is a Registered Pension Scheme for the purposes of the Finance Act 2004.

30. The Trustees may hold insurance policies or other assets that are earmarked for the benefit of certain members, for instance immediate annuity policies purchased to match all or part of the Plan liabilities, or benefits secured by Additional Voluntary Contributions, Individual Transfers in or Special Payments.

31. The Trustees recognise a number of risks involved in the investment of the Plan's assets, and, where applicable, monitors these risks in conjunction with the Fiduciary Manager.

Deficit risk:

Solvency risk and mismatch risk:

Investment Manager risk:

Liquidity risk:

Credit risk:

Currency risk:

Interest rate and inflation risk:

Political risk:

Sponsor risk:

Legislative risk:

32. The measures do not render the investment policy free of risk. Rather, the measures endeavour to balance the need for risk control and the need to allow the investment managers sufficient flexibility to manage the assets in such a way as to achieve the required performance targets. The risks detailed above will be monitored on a regular basis.

Adopted by the Trustees of the Matheson Group Pension Plan in June 2024, replacing the previous SIP dated July 2023.

Why have we produced this Statement?

The Trustees of The Matheson Group Pension Plan have prepared this statement to comply with the requirements of the Occupational Pension Plans (Investment and Disclosure) (Amendment) Regulations 2019.

This statement sets out how the Trustees have complied with the voting and engagement policies detailed in the Plan’s Statement of Investment Principles (SIP).

A copy of the SIP can be found at Pension plan - Statement of investment princples tab.

What is the Statement of Investment Principles (SIP)?

The SIP sets out key investment policies including the Trustees’ investment objectives and investment strategy.

It also explains how and why the Trustees delegate certain responsibilities to third parties and the risks the Plan faces and the mitigated responses.

The Trustees last reviewed the SIP in June 2024.

What is the purpose of this Statement?

What changes have we made to the SIP?

There were no changes made to the SIP over the year.

Why does the Trustees believe voting and engagement is important?

The Trustees' view is that Environmental, Social and Governance ("ESG") factors can have a potential impact on investment returns, particularly over the long-term and therefore contribute to the security of members' benefits.

The Trustees further believe that voting and engagement are important tools to influence these issues.

The Trustees have appointed a Fiduciary Manager who shares this view and considers and integrates ESG factors, voting and engagement in its processes.

The Trustees incorporate an assessment of the Fiduciary Manager's performance in this area as part of its overall assessment of the Fiduciary Manager's performance.

What are the Trustees’ voting and engagement policy?

When considering its policy in relation to stewardship including engagement and voting, the Trustees expect investment managers to address broad ESG considerations, but has identified climate change, and human and labour rights as areas of focus.

The day-to-day integration of ESG considerations, voting and engagement are delegated to the investment managers. The Trustees expect investment managers to sign up to local Stewardship Codes and to act as responsible stewards of capital.

Where ESG factors are considered to be particularly influential to outcomes, the Trustees expect the Fiduciary Manager to engage with investment managers to improve their processes.

What are the Fiduciary Manager's policies?

Climate change and net zero goal

The Trustees believe Climate Change is a current priority when engaging with public policy, investment managers and corporates.

The Fiduciary Manager has a goal to achieve net zero greenhouse gas emissions across 'In Scope Solutions' by 2050. They believe the trajectory is important, so are also aiming to approximately halve emissions per amount invested by 2030.

Public policy and corporate engagement

The Fiduciary Manager employs an external stewardship service provider, whose services include public policy engagement, and corporate voting and engagement on behalf of its clients (including the Trustees).

Some highlights from 2024 include:

Industry initiatives

The Fiduciary Manager participated in a range of industry initiatives over the year to seek to exercise good stewardship practices.

Please refer to their latest UK Stewardship Code for more information.

How does the Fiduciary Manager assess the investment managers?

Investment manager appointment

The Fiduciary Manager considers the investment managers’ policies and activities in relation to ESG factors and stewardship (which includes voting and engagement) at the appointment of a new manager. In 2024 the Fiduciary Manager conducted engagements with over 70 managers across asset classes. They also engaged over 100 products on sustainability and stewardship. In addition, over 150 sustainability‑theme strategies were researched.

Investment manager monitoring

The Fiduciary Manager produces detailed reports on the investment managers’ ESG integration and stewardship capabilities on an annual basis.

Investment manager termination

The Fiduciary Manager engages with investment managers to improve their practices and increases the bar by which they are assessed as best practice evolves.

The Fiduciary Manager may terminate an investment manager’s appointment if they fail to demonstrate an acceptable level of practice in these areas. However, no investment managers were terminated on these grounds during the year.

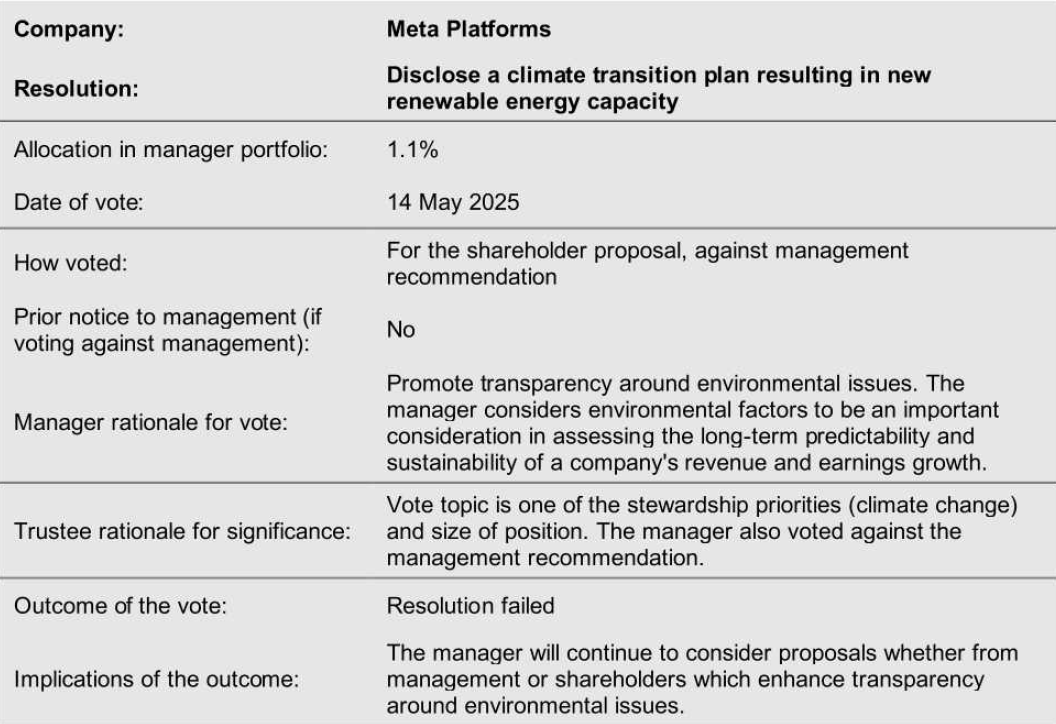

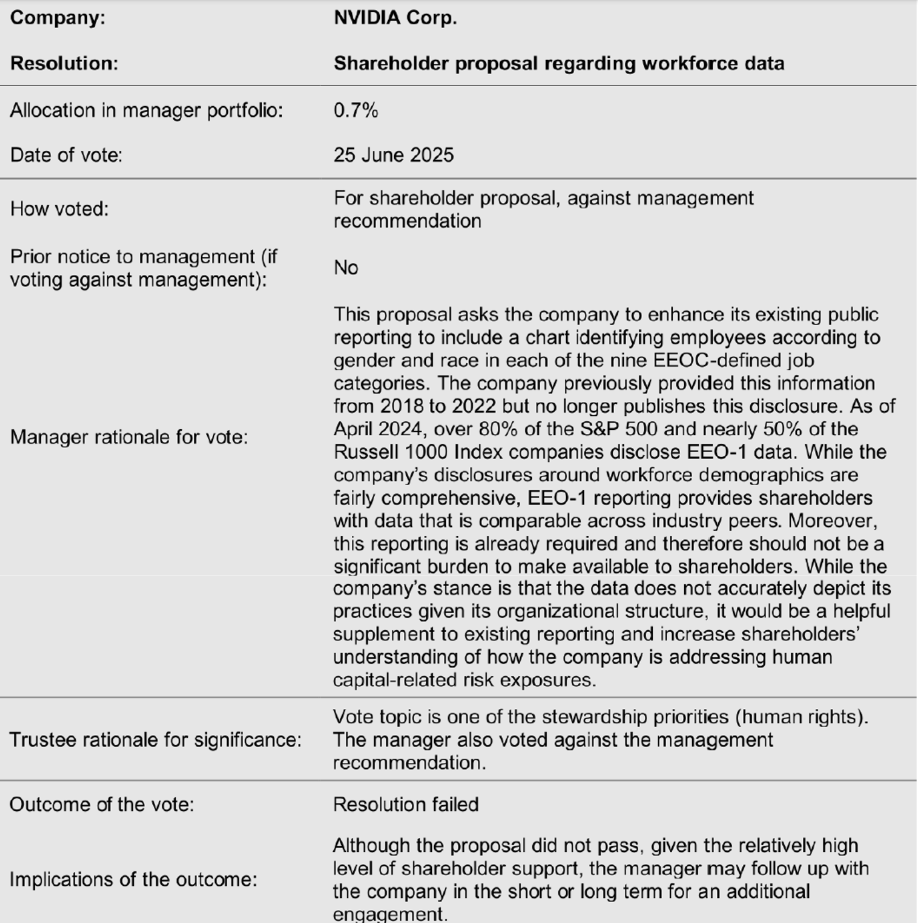

Example of engagement carried out over the year

Infrastructure manager

Climate Change – Climate reporting issue

Issue: This investment manager is a leading investor, developer, and long-term manager of core infrastructure assets. This engagement formed part of the Fiduciary Manager’s annual Sustainable Investment (SI) review of the manager, in alignment with its broader investment approach. SI engagement emphasises transparency, climate risk management and alignment, for example with global sustainability goals like SDG 13: Climate Action. The engagement was prompted by gaps identified in ESG reporting, including the absence of data on climate solutions and limited carbon emissions or footprint data; limited disclosure of carbon reduction targets; and further detail sought for the work the firm was undertaking in the area of climate-related risks.

Outcome: The manager acknowledged that, while not all their funds had completed the EU Taxonomy alignment process, eligible climate solutions were present in portfolios and would be better reflected in future disclosures. The firm published TCFD-aligned reports in 2024 using PCAF data and is working to improve asset-level data collection for future reporting. It also committed to set portfolio-level carbon reduction targets, following the firm-wide ambition set in 2024. On climate risk, the manager has partnered with industry specialists to be at the vanguard of understanding this area. It is developing a more advanced approach to assess materiality and financial impact on the assets in which the firm has invested.

Looking ahead, the manager agreed that the Corporate Sustainability Reporting Directive (CSRD) is going to be a component of reporting in 2025 as a number of assets fall into scope. It has also commissioned a portfolio decarbonisation study focused on social infrastructure concessions, a more challenging area of the infrastructure opportunity set. A key priority going forward is improving the quality and consistency of carbon emissions and footprint data across their portfolios, an effort which remains ongoing.

Emerging market equity manager

Climate change - Water security issue

Issue: Water security is important for businesses and society, and hence a financial risk for investors. In South Africa, water risk is a thematic area of focus for this particular asset manager. As part of its engagement, the manager requested information from companies, including disclosure of water consumption or withdrawal data, and details on processes and controls for assessing water-related risks and responding to water loss events. Additionally, the manager wanted to understand how companies are managing water risks, and companies’ water risk management policies and water reduction targets.

In 2023, the manager assessed water risks across the Johannesburg Stock Exchange Top 100, analysing disclosures, reduction targets, and penalties, while engaging with 58 companies. By 2024, the manager refined the analysis to 31 high-risk companies based on water usage, sector risks, and regional stress. They then analysed their public disclosures to identify gaps in oversight, mitigation strategies, targets, risk assessment, and supplier engagement. Using these insights, they assessed overall water risk management and developed tailored engagement questions for 19 companies with remaining concerns.

Outcome: One investee company confirmed exposure to water stress in three sites and outlined mitigation efforts including efficiency improvements, expanded water reuse, and a targeted reduction by 2030. The company acknowledged the regional initiative to lower water consumption and plans to participate in a project to enhance water security.

Overall, these discussions strengthened the manager’s understanding of municipal water management efforts and informed ongoing engagements with companies on water-related risks, which may be financially material.

Secure Income manager

General ESG issue

Issue: As part of the annual ESG review, the manager focused on addressing key deficiencies identified during the previous engagement. These deficiencies included the lack of a dedicated Inclusion and Diversity (I&D) resource, the absence of climate scenario and Climate Value-at-Risk (CTVaR) analysis for underlying assets, and the lack of disclosure for carbon emissions at both the firm and fund levels.

Outcome: The manager has made significant strides in addressing key areas of improvement. The lack of a dedicated I&D resource has been mitigated by establishing a management committee specifically responsible for Diversity, Equity, and Inclusion (DEI). Additionally, a separate workstream has been initiated to develop a comprehensive DEI strategy, which includes a thorough review of current policies.

The absence of CTVaR and climate scenario analysis for underlying assets is being tackled on a firmwide level. For the Solar II project, a provider has been engaged during the due diligence phase of potential investments. The team is currently in the process of evaluating various providers and aims to finalize their selection by the end of the year.

While there has been no disclosure of firm or fund-level carbon emissions previously, the manager has now reported firm-level emissions. Although Scope 3 emissions are still pending, efforts are actively underway to address this gap.

What are the voting statistics we provide?

The Plan is invested across a diverse range of asset classes which carry different ownership rights, for example bonds do not have voting rights attached. Therefore, voting information was only requested from the Plan’s equity investment managers.

Responses received are provided in the following pages. The Trustees used the following criteria to determine the most significant votes:

The Plan is invested in both active (trying to outperform the market) and passive (aiming to perform in line with the market) equity funds.

How have our Investment Managers voted over the last 12 months?

Towers Watson Partners Fund

Pooled multi‑asset growth fund

How many votes has this manager cast?

What is this manager’s voting policy?

As the manager manages Fund of Funds, the voting rights for the holdings are the responsibility of the underlying managers. The manager expects all their underlying managers who hold equities over a reasonable timeframe to vote all shares they hold. The manager has appointed EOS at Federated Hermes (EOS) to provide voting recommendations to enhance engagement and achieve responsible ownership. EOS also carries out public policy engagement and advocacy on behalf of all their clients. In addition, EOS is expanding the remit of engagement activity they perform on the manager’s behalf beyond public equity markets, which will enhance stewardship practices over time.

Underlying managers are required to provide a detailed explanation and rationale whenever their voting decisions diverge from the EOS recommendations. They also utilise Institutional Shareholder Services (ISS) for voting facilitation and research purposes. Additionally, their China equity manager employs the Glass Lewis service, utilising a bespoke policy. Their emerging markets equity managers use ISS, Glass Lewis, SES and Broadridge Proxy Edge platforms for information and to facilitate voting. Meanwhile, their long‑short equity managers use ISS to provide corporate research and to facilitate the voting process.

Which of these votes do you think were significant?

In conclusion…

The Trustees are satisfied that over the year, all SIP policies and principles were adhered and in particular, those relating to voting and engagement.

Matheson & Co., Limited

12 Upper Grosvenor Street

London, Mayfair

W1K 2ND

United Kingdom

Tel: 020 7816 8100

Email: enquiries@matheson.co.uk

Website: www.matheson.co.uk